This article was published in the Winter 2020 issue

by Dan Rees, Partner, Latham & Watkins

Special purpose acquisition companies, or SPACs, have seen a significant uptick in 2020 both in volume of initial public offerings (IPOs) and in capital raised. This increase, the involvement of well-known investment professionals in SPAC formations in a broader array of sectors, and the increased flexibility in SPAC business combination terms coupled with increased market volatility has given more private companies reasons to consider a SPAC transaction as a path to go public.

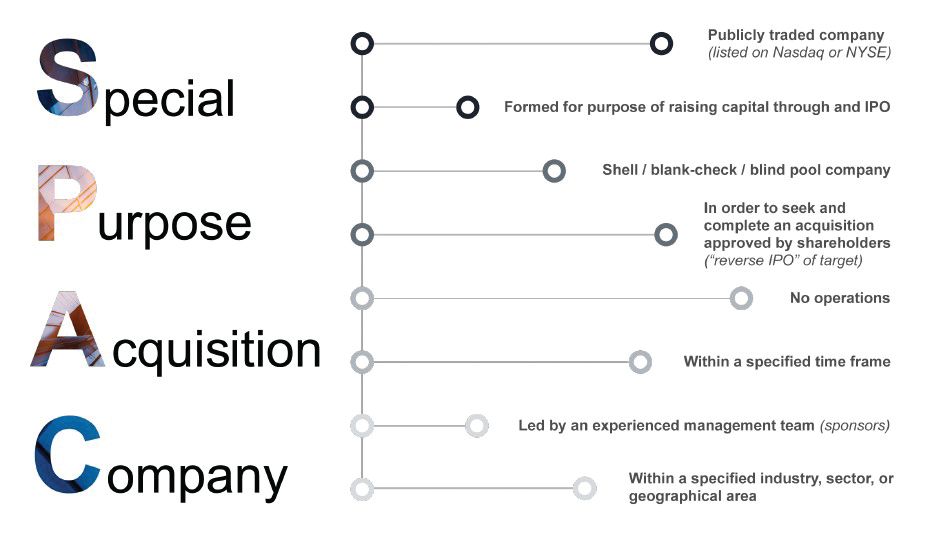

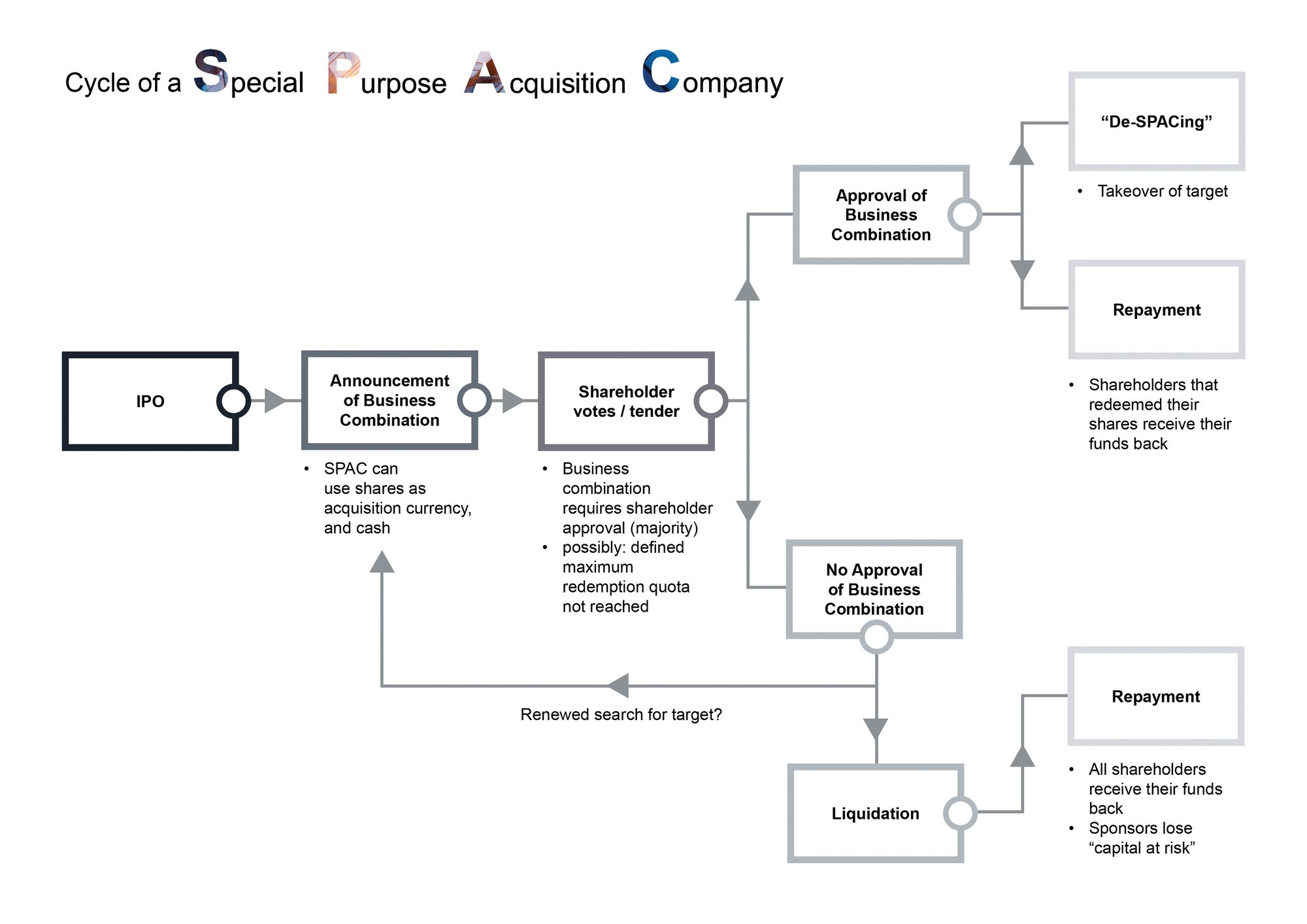

What is a SPAC? A SPAC is an entity formed solely to raise capital through an IPO without any commercial operations for the purpose of acquiring an existing company. SPACs are generally formed by investors, or sponsors, with expertise in a particular business sector, with the intention of pursuing business combinations. Upon completion of an IPO, a SPAC typically has two years to complete a business combination with an existing company, or face liquidation. Companies aiming to go public through a SPAC transaction are typically one to five times larger in value than the SPAC partner.

Why a SPAC transaction? A primary advantage for a private company of a SPAC transaction over other paths to the public market is the relative speed. A company can typically transition from identification of a SPAC partner to completion of a transaction in around four to six months. In addition, a SPAC transaction allows the company to negotiate valuation with a single party, providing greater pricing certainty than an IPO. A SPAC transaction can also allow for more creative terms and deal structuring than an IPO. For example, SPAC transactions offer the option to raise significantly more capital than the 10 – 15% stake available in an IPO and can allow for immediate liquidity for company stockholders. A SPAC transaction also allows the company to disclose financial projections which it would not have the ability to do in a traditional IPO.

With certain advantages SPAC transactions can offer, there are other factors to be considered. There is significant dilution associated with economics granted to management of the SPAC along with governance rights to be negotiated with the sponsor. The redemption rights of SPAC investors can also add uncertainty to the amount of cash that will be available to the company at closing, though this can be partially backstopped through mechanisms such as a concurrent public investment in private equity, or PIPE.

If you are considering going public through a business combination with a SPAC, attributes that can increase the success of the transaction include working with a sponsor with a track record and brand name recognition, understanding the investor base of the SPAC and early public readiness. Latham has represented both private companies and SPACs in some of the most significant SPAC IPO and business combination transactions globally. We offer a full-service team to advise you on the process and life as a public company.

Take Our Survey

Hi! The Silicon Slopes team is interested in your feedback. We are asking for a couple minutes to quickly provide feedback on our Silicon Slopes quarterly magazine publication. Click HERE and share your thoughts with us. Your responses will help us improve. Thanks!

*Read the latest issue of Silicon Slopes Magazine, Winter 2020

{kind=link}