The No. 1 SBA loan originator in Utah with nearly $500 million in total loans outstanding and more than $735 million in deposits, Rock Canyon Bank and its seven branches is valued at 10.4X projected 2023 earnings per share. But it’s the SBA loan practices of Rock Canyon Bank that have the potential to produce the greatest benefits to its acquiror: National Bank Holdings.

Utah’s top originator of U.S. Small Business Administration loans is being acquired.

That was the news coming out of Denver, Colorado, early yesterday afternoon when National Bank Holdings (NYSE:NBHC) announced its first quarter results and disclosed at the same time that it is buying Provo, Utah-based Community Bank, parent company of Rock Canyon Bank, for $136 million in cash and stock.

According to terms disclosed Monday about the definitive agreement, National Bank Holdings is paying approximately $16.1 million in cash and approximately 3.1 million in NBHC shares to acquire CB/Rock Canyon.

Based upon a closing price of $38.69 for NBHC shares on Friday, April 14, the transaction valuation is roughly $136 million.

This provides a cash vs. stock mixture of approximately 12% vs. 88% for the purchase.

According to the NBHC investor presentation published yesterday afternoon—NBHC To Acquire Rock Canyon Bank—the acquisition of CB/Rock Canyon is priced at 10.4X its projected 2023 earnings per share.

Interestingly, NBH announced on April 1st it was acquiring Bancshares of Jackson Hole Incorporated (aka, Bank of Jackson Hole) and its 12 banking centers in Wyoming and Idaho for approximately $230 million in cash and stock.

As a result, after closing the CB/Rock Canyon and Bank of Jackson Hole acquisitions, NBH Bank, the operating subsidiary of National Bank Holdings, will have four subsidiaries with over 100 locations in eight states:

- Bank of Jackson Hole (Idaho and Wyoming),

- Bank Midwest (Kansas and Missouri),

- Community Banks of Colorado, and

- Hillcrest Bank (New Mexico, Texas, and Utah).

[NOTE: Rock Canyon Bank will apparently be rebranded post-acquisition and folded into Hillcrest Bank.]

According to the NBHC/CB investor presentation, Rock Canyon Bank investors have already voted in favor of the acquisition and RBHC shareholder approval is not required.

In other words, this is a done deal.

So barring any unforeseen regulatory challenges, the acquisition of CB/Rock Canyon Bank is expected to close in the second half of 2022.

CB/Rock Canyon Bank Acquisition Analysis

CB/Rock Canyon Bank is a community bank that was formed in 1991, and it has seven branches today in Fillmore, Lehi, Orem, Pleasant Grove, Provo, Spanish Fork, and St. George.

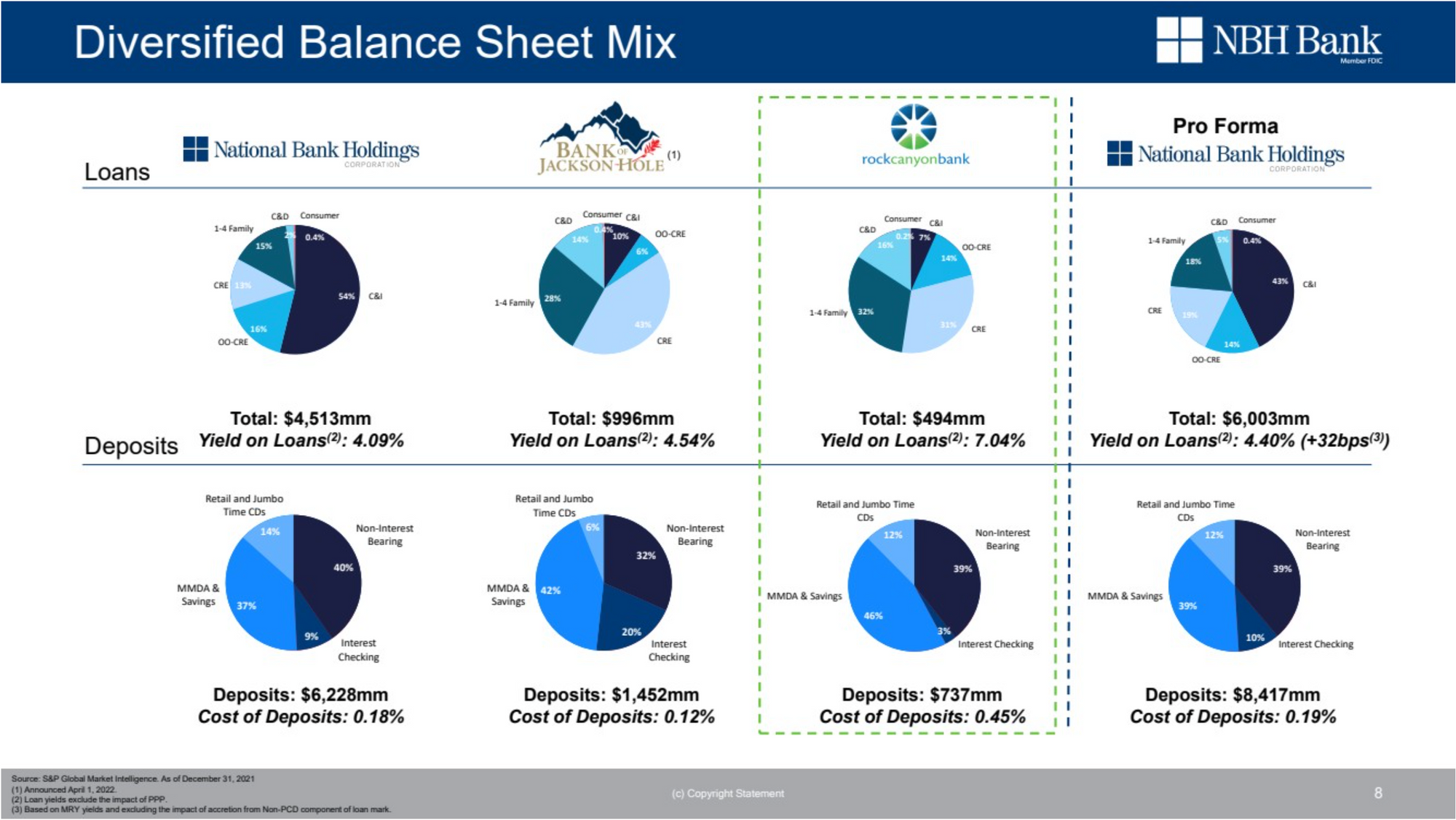

In total, Rock Canyon Bank has $814 million in assets, deposits of $737 million, and $494 million in loans outstanding.

Where the Rock Canyon Bank story gets interesting, however, is when you dig into the numbers.

Specifically, as noted above, Rock Canyon Bank is the No. 1 originator of Small Business Administration loans in the state of Utah, including 504, 504 refinance, 7(a), FSA, and USDA loans.

However, where NBH Bank is currently producing returns of 4.09% on its loans, Rock Canyon Bank is generating a yield of 7.04% for its loan portfolio, an increase of over 72% of what NBH Bank is generating presently.

At just under $500 million in loans, Rock Canyon Bank falls shy of 11% of the total loan amount currently held by NBH Bank.

But a 72% difference in loan yield is still a huge jump, and depending upon the internal loan processes of Rock Canyon Bank, they may provide some intriguing benefits to NBHC and its shareholders.

Case in point, based upon the figures in the NBHC/CB investor deck, National Bank Holdings expects to see its loan yield jump to 4.4% after closing both the Bank of Jackson Hole and CB/Rock Canyon Bank acquisitions later this year.

That’s not shabby, as it would mean that on a pro forma basis at $6 billion in combined loan balances, NBH Bank would see its annual loan yield jump to slightly over $264 million vs. the $245 million it would produce using its pre-acquisitions loan yield figure of 4.09%.

But, what happens if NBH Bank is able to crack the code CB/Rock Canyon Bank is using to produce loan yields that are 72% higher at 7.04% per loan? Well, that’s when things get crazy:

Instead of producing a return of $264 million on loans totalling $6.0 billion, NBH Bank would generate an annual return of over $422 million, a gross increase of more than $158 million–merely by achieving the same results Rock Canyon Bank is producing.

To put this pie-in-the-sky $158 million increase in perspective, remember that NBHC is only paying $136 million for CB/Rock Canyon Bank.

In other words, achieving such loan yield results portfolio-wide would mean that such a process transformation would completely pay for the CB/Rock Canyon Bank acquisition in under 12 months.

Does NBHC/NBH Bank expect to do this?

Apparently not, at least not according to its investor presentation, as shown on the slide above.

But the prospect is intriguing.

However, according to Tim Laney, chairman, president and CEO of National Bank Holdings Corporation,

“Rock Canyon Bank’s highly successful SBA business strategy de-risks the balance sheet, produces strong fee income, and is scalable across our franchise. Equally important, this acquisition strengthens our position as a premier regional bank serving the fast-growing Salt Lake City region.”

Did you catch that?

“(The Rock Canyon Bank) SBA business strategy … is scalable across our franchise.”

Hmmmmm. Very interesting.

A Final Acquisition Thought

Beyond this, however, there was another interesting tidbit tucked away within the NBHC/CB investor deck.

That’s the fact that the costs of Rock Canyon Bank’s deposits (aka, the interest it pays to its depositors) is 2.5 times higher than the amount NBH Bank is paying out to its depositors.

Unfortunately, the ability of NBH Bank to bring Rock Canyon Bank’s deposit interest rates in line with its own is a lot trickier, especially given depositor demographic and psychographic variability from subsidiary to subsidiary and from one region of the country to another.

And even if it did, Rock Canyon Bank deposits come in at just 11.7% of the amount of NBH Bank deposits: $737 million versus $6.3 billion.

So even if the Rock Canyon Bank deposit mixture and costs came in line with those of NBH Bank, the deposit cost savings would only be approximately $2 million, which is not nothing—but it’s not significant either, per se.

Bottom line, though relatively small asset-wise in comparison to NBH Bank, Rock Canyon Bank has the potential to have an outsize impact on its larger acquiror, especially because of its SBA loan business practices.

{kind=link}